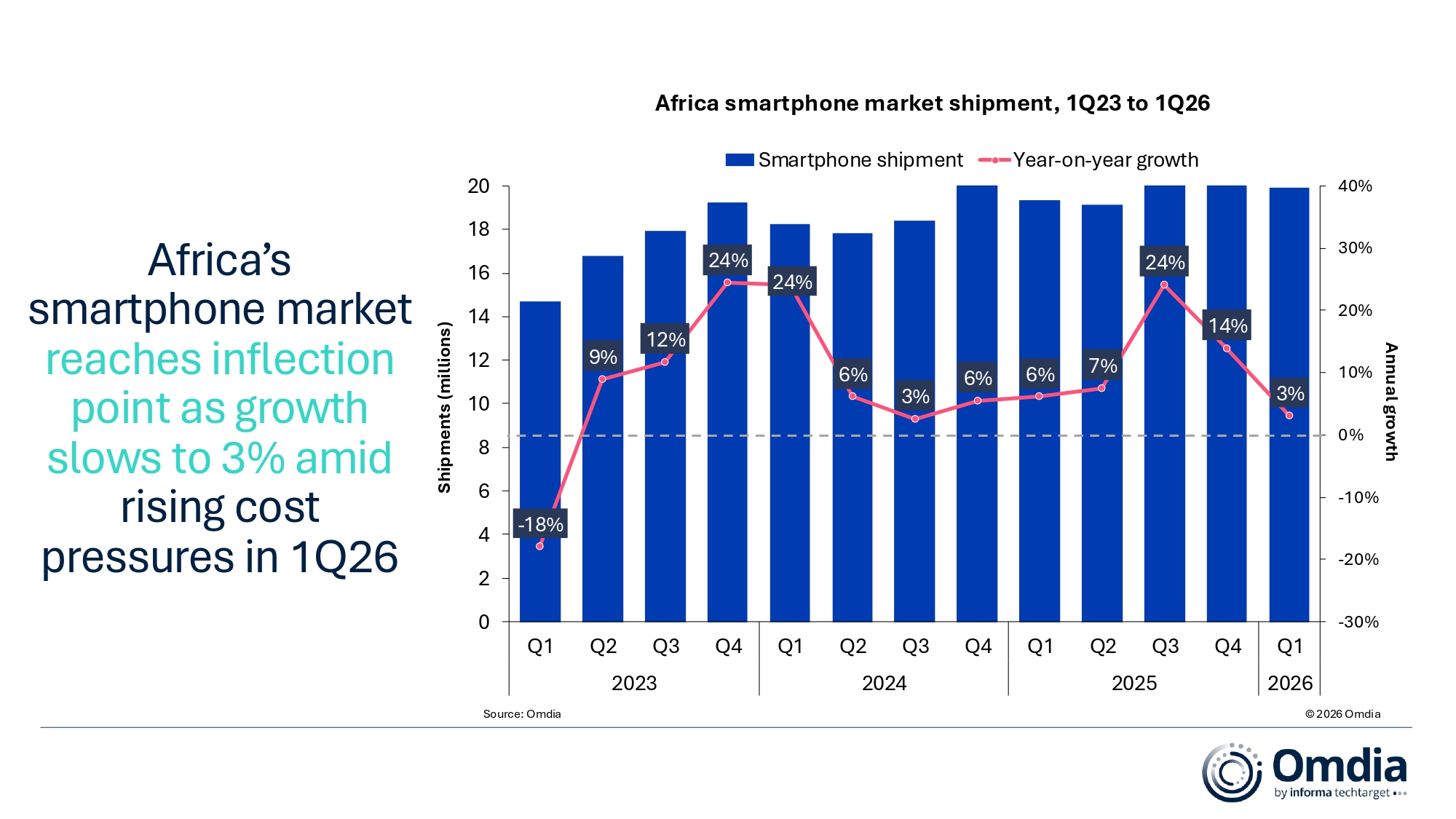

Omdia: Africa Smartphone Shipments Up 3% in Q1, 2026 Outlook Cut 28%

Omdia’s latest research shows Africa’s smartphone shipments grew 3% year on year to 19.9 million units in 1Q26, supported by new product launches and inventory frontloading by top vendors. Despite the modest growth, market conditions continued to weaken across many African economies amid rising component prices, currency volatility, and broader affordability pressures in the region’s dominant sub-US$150 segment. Notably, underlying demand across Africa remains structurally strong, driven by expanding connectivity needs, adoption of digital services and a young, mobile-first population. However, worsening economic and operational headwinds are making smartphone affordability increasingly challenging for both consumers and vendors.

South Africa was among Africa’s strongest-performing smartphone markets in 1Q26, growing 17% year on year as replacement demand and higher-value smartphone purchases remained resilient. ASPs rose 4% to US$369, led by Samsung’s premium ecosystem and HONOR expansion in the upper mid-range segment. Nigeria grew 8% year on year in 1Q26, supported by resilient demand for affordable 4G and 5G smartphones, particularly in the US$200–299 segment, as consumers prioritized connectivity despite ongoing economic pressures and rising data costs.

Elsewhere, market conditions remained challenging across several African economies. Egypt declined 10% amid weaker consumer sentiment and supply chain disruptions linked to broader geopolitical tensions in Middle East, while Kenya fell 16% as rising retail prices pushed consumers to extend replacement cycles significantly. Algeria recorded the region’s steepest decline, down 28%, as stricter import regulations, forex constraints and delays in full scale local manufacturing expansion disrupted short-term smartphone supply. Morocco emerged as one of the quarter’s positive surprises, growing 6% after import duties were reduced to 2.5% from 17.5%, helping improve retail momentum and device affordability.

“Escalating memory input cost continues to build pricing pressure on vendors, while financing-led demand is gradually improving accessibility to higher-priced devices,” said Manish Pravinkumar, Principal Analyst at Omdia. “”The sub-$200 segment retained 75% of 1Q26 shipments, yet cost-push pressure compelled vendors to reprice and reposition their lineups toward higher bands — the 43% expansion of the US$300–499 segment is the clearest evidence of this structural shift, cushioned by stronger financing programs.”

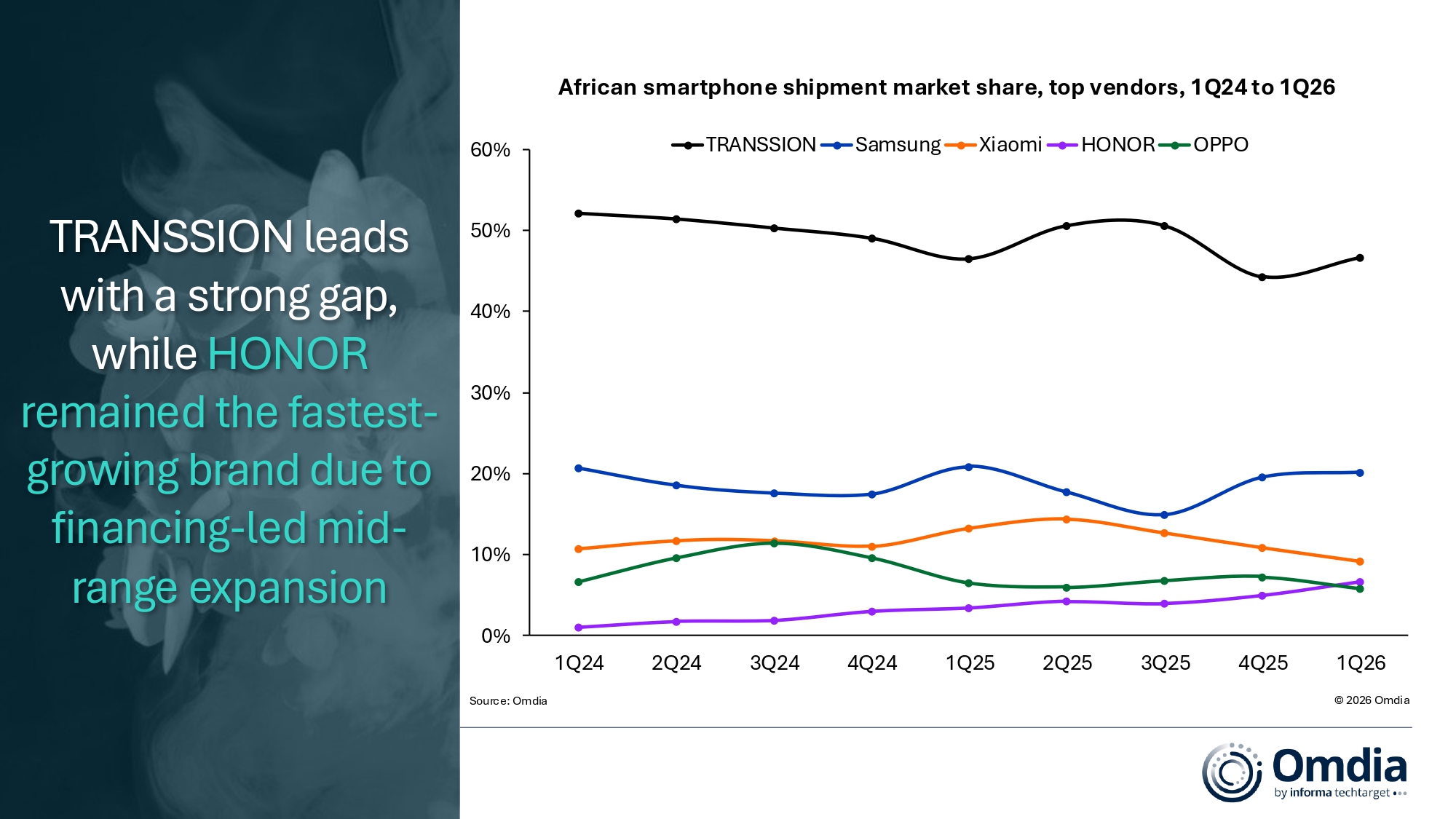

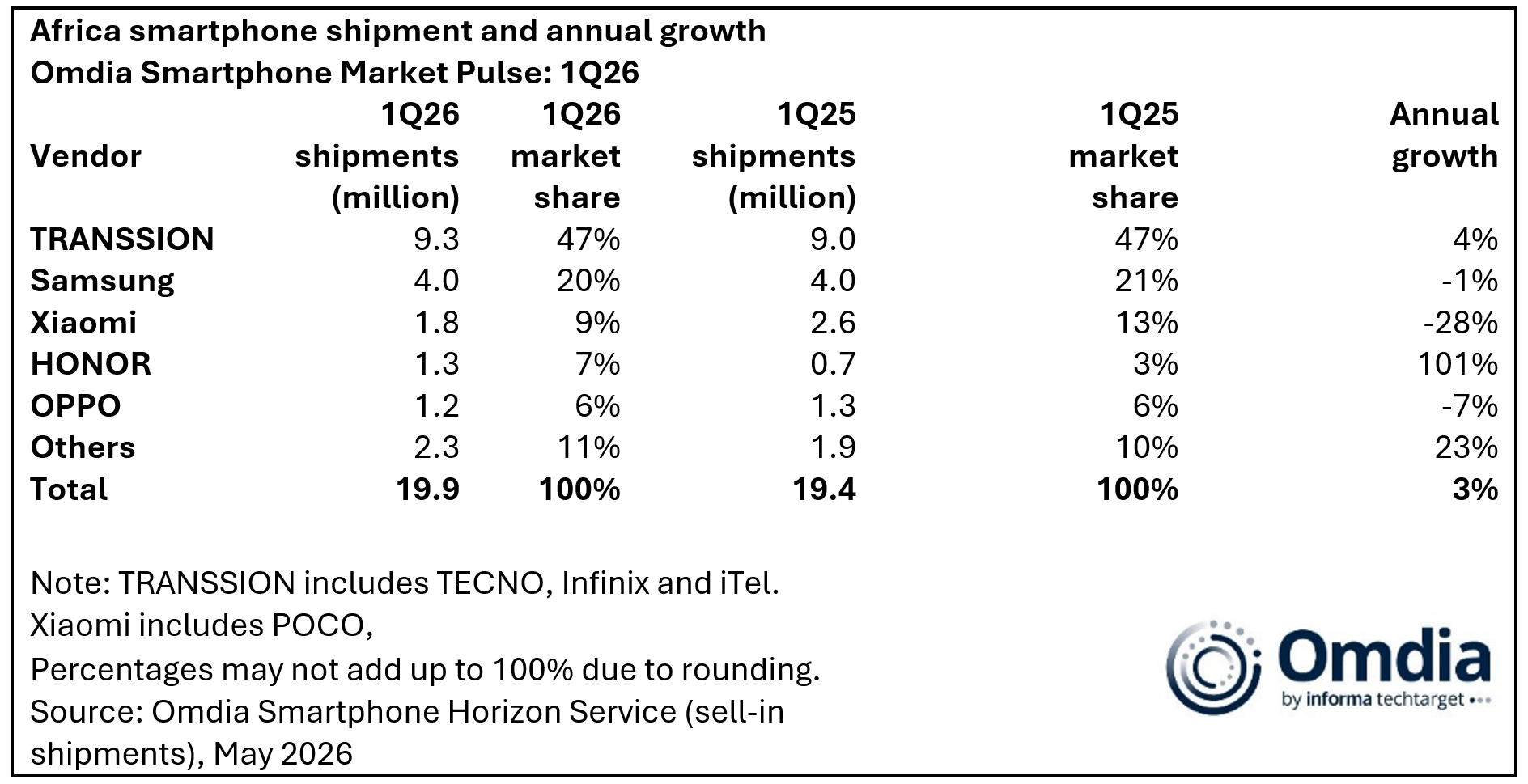

“TRANSSION retained the top spot with a 47% share and 4% growth, supported by disciplined inventory management and continued strength in affordable models such as the Tecno Pop 10 and Spark 40C 4G. Samsung recorded a marginal 1% decline, with the Galaxy A-series continuing to dominate the critical US$150–299 segment, while its localized distribution investments in Egypt remain strategically important for the long term. HONOR saw the strongest annual growth of 101%, supported by South Africa’s operator-led mid-range market and stronger financing-led demand. Xiaomi shipments fell 28% year on year as memory supply constraints hindered its aggressive entry-tier strategy despite a gradual portfolio shift toward higher-priced devices. OPPO declined 7% amid ongoing operational restructuring and weaker market conditions in Egypt.”

“Africa’s ultra-affordable smartphone market is entering a structurally more challenging phase in 2026 as margin compression strains entry-tier device economics to a breaking point,” concluded Pravinkumar. “Omdia forecasts a 28% contraction in 2026 as memory inflation, elevated supply chain costs and deepening purchasing power constraints bear down on the sub-US$200 segment at the core of Africa’s market, and most acutely in the US$80–150 tier — the price band that built Africa’s smartphone adoption story, pushing the region’s next wave of digital adoption further beyond earlier 2026–2027 expectations.”

“Looking ahead, the widening competitive gap between scale-driven market leaders and the challenger tier will be one of the defining narratives of the second half of 2026. Vendors with established financing ecosystems, entrenched operator partnerships, localized manufacturing and extensive last-mile distribution will be best positioned to sustain device accessibility and protect volumes as market conditions tighten further.”